Clarity Through Complexity: Bonds Take Center Stage

Relief, Not Resolution

While the threat of Liberation Day 2.0 — a wave of new tariffs and global trade frictions — continues to loom, policymakers have so far tapped the brakes. Recent signals out of Washington suggest a more measured approach to trade, with delayed implementations and softer rhetoric replacing earlier saber-rattling. That was enough to ignite a powerful equity rally, as the S&P 500 surged nearly 11% in Q2, reaching all-time highs.

But amid the headlines and stock market recovery, we believe the more important story lies in the fixed income markets, where shifting dynamics are creating both challenges and opportunities.

The Bond Market Is Back – And More Complicated Than Ever

With higher interest rates sticking around longer than expected, and the yield on the 10-year Treasury hovering above 4.2%, bonds are again proving their value as a core part of a diversified portfolio. Yet the bond market today is very different than it was just a few years ago — and requires a more nuanced approach.

At LA Wealth, we’ve been mindful of these shifts, particularly:

- How much U.S. government debt we hold

- Where we seek yield

- And how we diversify across global credit markets

Here’s what we’re paying attention to and how it impacts your portfolio.

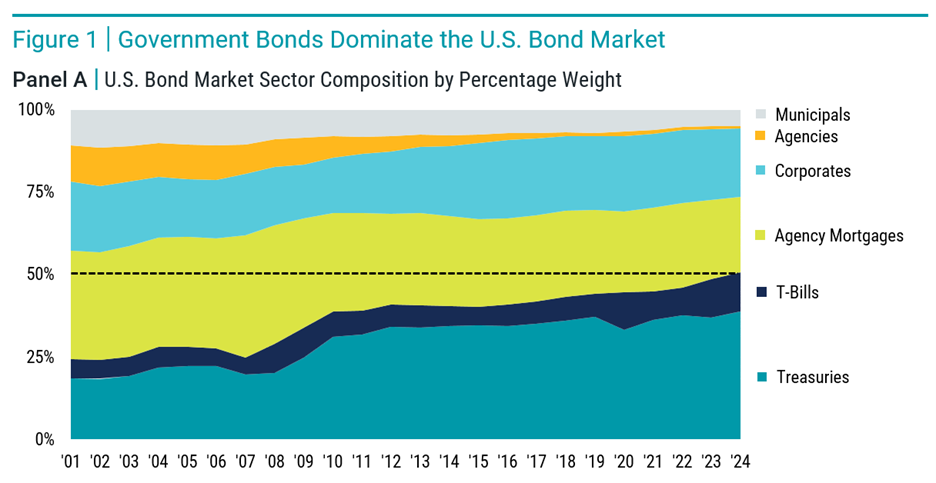

1. Treasuries Now Dominate – But We’re Selective

Today, U.S. Treasuries make up nearly 50% of the U.S. bond market, up from just 25% in 2001. When you include agency-backed and mortgage securities, more than 70% of the bond market is tied to government debt.

This concentration has real implications. While Treasuries are considered safe, they also reflect a growing national debt load and carry increased interest rate sensitivity, especially with long-term yields now flirting with 5%.

We’ve been intentional in not allowing our portfolios to overexpose clients to government debt. Instead, we seek balance by diversifying into credit sectors that offer better return potential without taking on undue risk.

*Data from 2001 – 2024. Source Bloomberg. Municipals are bonds issued by municipalities such as states, cities, and counties. Corporates are debt instruments issued by corporations, as distinct from those issued by governments, government agencies or municipalities. Agency Mortgages are mortgage-backed securities typically issued by U.S. government agencies.

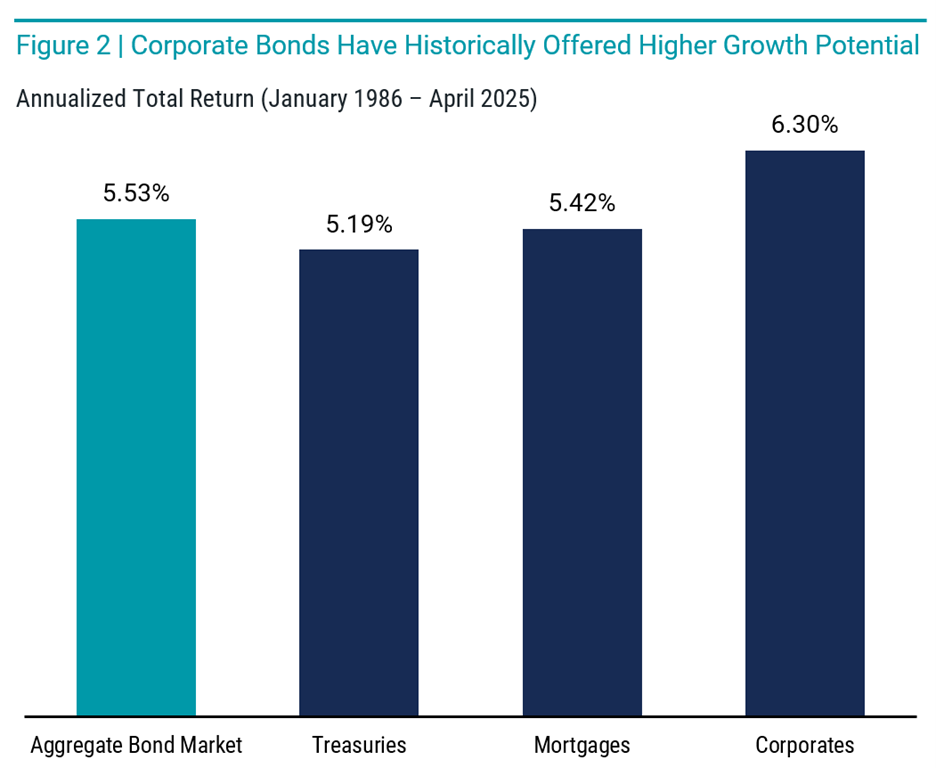

2. Corporate Bonds: Attractive Yields Without Excessive Risk

For long-term investors, corporate bonds have historically delivered stronger returns than government bonds, returning 6.3% annually since 1986 versus 5.2% for Treasuries. And while corporate debt may sound riskier, the data tells a different story: default rates for investment-grade and even BB-rated high-yield bonds have remained below 1% per year for over four decades.

That’s why our fixed income strategies continue to include meaningful exposure to high-quality corporate bonds and select high-yield segments, where we believe the risk-return trade-off is favorable, especially in a higher-rate environment.

Data from 1/1/1986 – 4/30/2025. Aggregate bond market is represented by the Bloomberg US Aggregate Bond Index. Treasuries, mortgages and corporates are represented by the individual sectors within that index. Source: Bloomberg, Avantis Investors.

Past performance is no guarantee of future results.

3. Going Global for Yield and Diversification

The U.S. may host the largest bond market, but it only represents 39% of global debt. In today’s environment, global corporate bonds — particularly those denominated in EUR, GBP, and CAD — offer attractive yields when hedged to USD, often exceeding U.S. equivalents.

Incorporating global bonds into portfolios helps reduce interest rate risk, smooth out volatility, and uncover new opportunities. Diversification across currencies, economies, and yield curves is a powerful way to build resilience in uncertain times.

What This Means for You…

By combining a disciplined core allocation to high-quality bonds with selective exposure to higher-yielding credit and international issuers, we believe investors can:

- Earn better income without sacrificing stability

- Reduce overconcentration in U.S. debt

- Enhance long-term total return potential

Our bond portfolios are not static — they’re actively monitored to ensure they remain aligned with your goals, current conditions, and future outlooks.

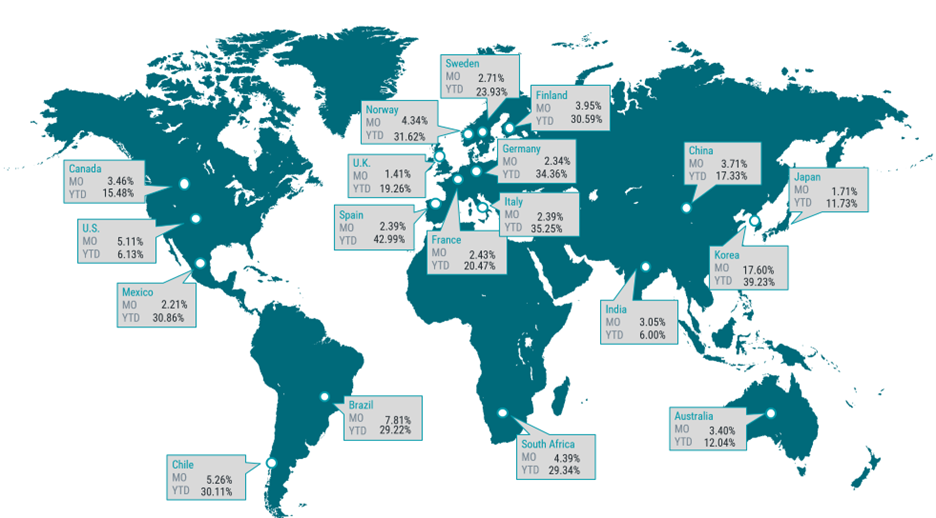

Equity Recap: Risk-On Returns, Especially Overseas

- The S&P 500 rebounded strongly in Q2, posting +10.9%, supported by strong corporate earnings and easing inflation pressures.

- Non-U.S. developed markets and emerging markets both outperformed for the quarter. Notably, Spain (+42.99%), Korea (+39.23%), and Italy (+35.25%) were standouts.

- Growth stocks led globally, but value names remain top performers year-to-date in several regions.

This reinforces our conviction in globally diversified equity allocations, even when U.S. headlines dominate the news.

Data as of 6/30/2025. Performance in USD. Past performance is no guarantee of future results. Source: FactSet. Countries are represented by MSCI country indices.

Closing Thoughts: Stay Anchored, Stay Intentional

It’s been a noisy year, from tariff threats to inflation whiplash to shifting central bank policies. But through it all, markets have proven resilient, and long-term portfolios that stayed disciplined have been rewarded.

As always, we remain focused on what we can control: thoughtful portfolio construction, data-driven decisions, and proactive risk management. We continue to believe that a flexible bond strategy, one that avoids complacency and seeks opportunity, is an essential part of your financial foundation.

Please reach out if you’d like to review your allocation, explore new fixed income strategies, or simply talk through the path ahead.

Diversification does not ensure a profit or guarantee against loss.

LA Wealth Advisors is a DBA of Axxcess Wealth Management, LLC a Registered Investment Advisor with the SEC. Advisory services are only offered to clients or prospective clients where Axxcess and its representatives are properly licensed or exempt from licensure.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.