“Perspective and Discipline Matter Most When Markets Test Patience”

Market Recap: A Quarter of Resilience and Rotation

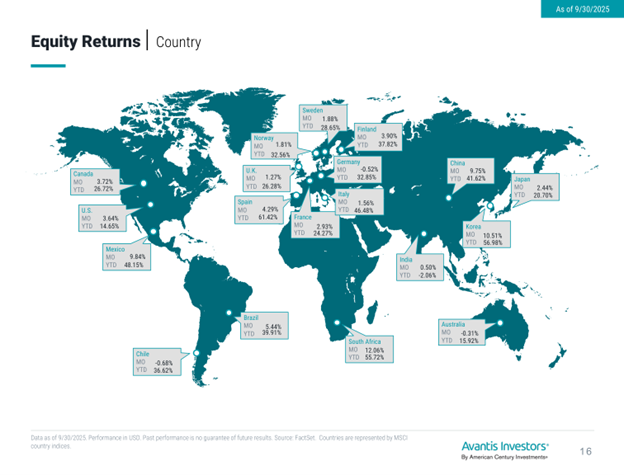

Data as of 9/30/2025. Performance in USD. Past performance is no guarantee of future results. Source: FactSet. Countries are represented by MSCI country indices.

Figure 1: Equity Returns by Country — Month-to-Date (MO) and Year-to-Date (YTD) (as of 9/30/2025)

Q3 2025 proved that markets can remain resilient even in the face of mixed economic signals. Equities advanced modestly—the S&P 500 rose around 2%—driven by persistent strength in large-cap growth and renewed interest in small-cap and value stocks.

Despite concerns around inflation “stickiness” and Fed hesitation on rate cuts, investors continued to price in a soft landing rather than a recession. Fixed income had a more muted quarter, as yields fluctuated near cycle highs. The 10-year Treasury hovered around 4.3%, creating headwinds for bond prices but opportunities for reinvestment at historically attractive yields.

Economic Themes to Watch

Inflation: Cooling, But Not Cold

Inflation is trending down but staying above the Fed’s 2% target. Core inflation remains driven by services and shelter costs. Expect gradual disinflation into 2026 as wage growth moderates and supply chains stabilize.

Earnings: Margins Stabilizing

Corporate profits surprised to the upside, particularly in technology and healthcare. Improving margins amid slower top-line growth suggest companies are adjusting effectively to higher rates and input costs.

Interest Rates and the Fed

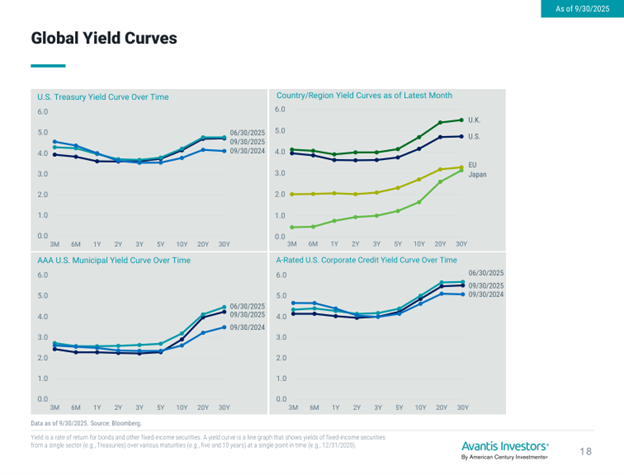

Data as of 9/30/2025. Source: Bloomberg. Yield is a rate of return for bonds and other fixed-income securities. A yield curve is a line graph that shows yields of fixed-income securities from a single sector over various maturities at a single point in time.

Figure 2: Global Yield Curves — U.S. Treasuries, Country/Region Sovereigns, AAA U.S. Municipals, and A-Rated U.S. Corporates (as of 9/30/2025)

The Fed held rates steady for a fourth consecutive meeting, balancing strong employment with moderating inflation. Futures markets now imply one to two cuts in 2026. This environment supports select opportunities in short-to-intermediate duration bonds and dividend-focused equities.

Investment Implications

Equities

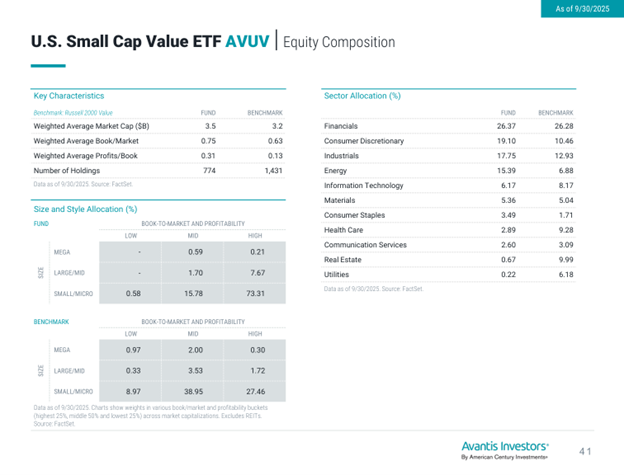

Data as of 9/30/2025. Source: FactSet.

Figure 3: Sector Allocation — U.S. Small Cap Value ETF (AVUV) vs. Benchmark (as of 9/30/2025)

Diversification remains crucial. International developed markets continue to offer attractive valuations relative to U.S. peers. Gradually rebalancing toward small-cap and international equities can enhance long-term return potential.

Fixed Income

Bonds are back as a meaningful source of income and stability. Active bond management can lock in yields without taking excessive duration risk.

Alternatives

Volatility in equities underscores the value of liquid alternatives and structured income strategies to buffer portfolios during uncertain rate environments.

Financial Planning Focus: Positioning for 2026

- Tax-loss harvesting: Use recent market volatility to offset gains.

- Retirement contributions: Maximize 401(k), SEP IRA, or Solo 401(k) deferrals before December 31.

- Roth conversions: If your income is lower this year, partial conversions may be more tax-efficient.

- Charitable giving: Donor-advised funds remain a powerful tool for both impact and tax planning.

Perspective: Staying the Course

Markets will always oscillate between optimism and fear. Successful investors tune out noise and stay aligned with their plan. Long-term investors are rewarded not for predicting the next move, but for staying invested through them.

Closing Thoughts

At LA Wealth Advisors, we continue to monitor both economic developments and your individual goals to ensure portfolios remain well-positioned. We appreciate your trust and partnership as we navigate these markets together.

— The LA Wealth Advisors Team

LA Wealth Advisors is a DBA of Axxcess Wealth Management, LLC a Registered Investment Advisor with the SEC. Advisory services are only offered to clients or prospective clients where Axxcess and its representatives are properly licensed or exempt from licensure.

This newsletter is for informational and educational purposes only and should not be construed as investment, legal, or tax advice. Please consult your financial, tax, or legal advisor regarding your individual circumstances.The charts and index data shown are presented for illustrative purposes only. Index performance does not represent the performance of any specific investment, and it is not possible to invest directly in an index. Past performance is no guarantee of future results. Market and economic conditions are subject to change without notice.

Sources include Bloomberg, FactSet, and Avantis Investors for the periods indicated. Opinions and estimates constitute judgment as of the date of this material and may change without notice. References to specific indices or securities, if any, are for illustrative purposes only and are not intended as recommendations to purchase or sell any security.Investments involve risk, including the possible loss of principal. Diversification does not ensure a profit or protect against loss in declining markets.

LA Wealth Advisors is a DBA of Axxcess Wealth Management, LLC a Registered Investment Advisor with the SEC. Advisory services are only offered to clients or prospective clients where Axxcess and its representatives are properly licensed or exempt from licensure.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.